Reverse Mortgage Rules

If you own a townhouse, condo, a manufactured home or a house built after or on July 15th, 1976, and then you might qualify to get a reverse mortgage. The Federal Housing Administration (FHA) prohibits cooperative housing owners from obtaining reverse mortgages from obtaining reverse mortgages because they own shares of the corporation and not the real estate they reside in.

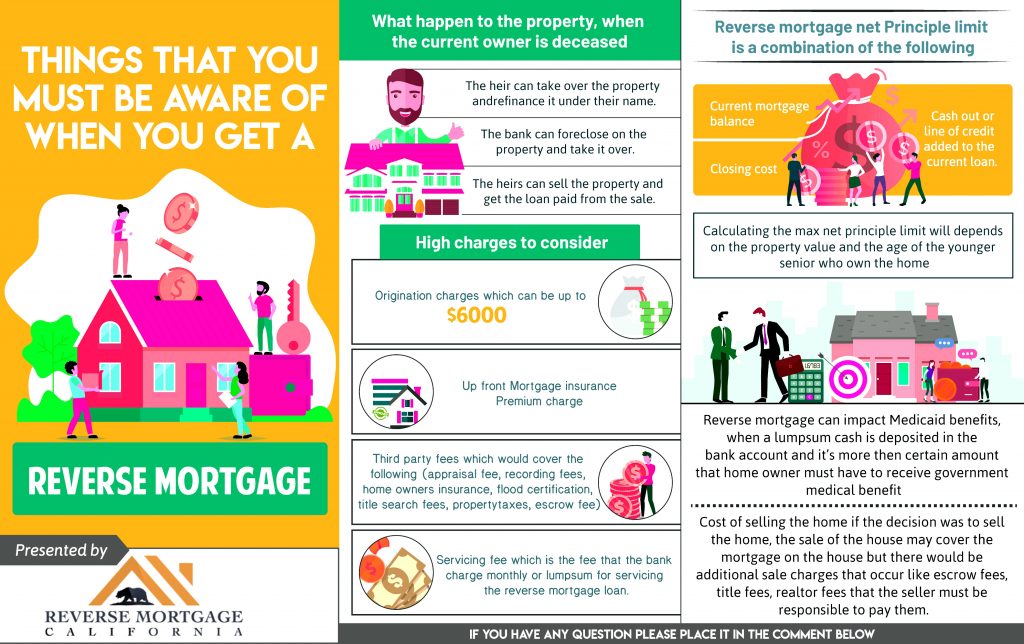

Although a reverse mortgage doesn’t have credit score or income requirements, there are for qualifications. You have to be 62 and above years of age, and must either own the home or have a significant amount of equity (50% and above). A borrower must pay loan servicing fees, an origination fee, interest, up-front insurance premium, and ongoing premiums for mortgage insurance. The amount lenders charge for these requirements is limited by the federal government

When the time comes to sell, lenders cannot go after the borrower or the heirs if the home is underwater. They must allow the heirs, if any some months to make a decision whether the lender should sell the home or if they will repay reverse mortgage.

All reverse mortgage borrowers must complete a HUD- approved counselling session as required by the Department of Housing and Urban Development (HUD). This counselling session n costs about $125. It should last at least I hour 30 minutes and discuss the cons and pros of getting a reverse mortgage given the unique personal and financial circumstances. It needs to explain the effects of a reverse mortgage on your eligibility for Supplemental Security Income and Medicaid. It should also cover the different ways to receive proceeds.

Under the rules of a reverse mortgage, your responsibilities as a borrower are to maintain your home in good condition, and pay all your homeowners insurance and property taxes on time. If you stop residing in the house for more than a year, even for medical reasons, you must repay the loan, usually attained by selling the home.

Even after recent reforms, the widower or widow can lose the house upon the death of their spouse in some situations. Scams that target the elderly is another risk in reverse mortgages.

Charges Involved

Since October 2017, insurance premiums provide funds for lenders if your loan balance becomes larger than the home value.

The upfront insurance premium is determined by the home’s value. For each $100000 appraised, you pay $2000.

Every borrower must pay an annual mortgage insurance premium of 0.5% (previously 1.25%) of the borrowed amount.

Lenders of Reverse Mortgage

Only specific lenders offer reverse mortgages. Some of the most popular reverse mortgage lenders include Liberty Home Equity Solutions, One Reverse Mortgage, and American Advisors Group.

You may check-in with various companies to compare the rates.