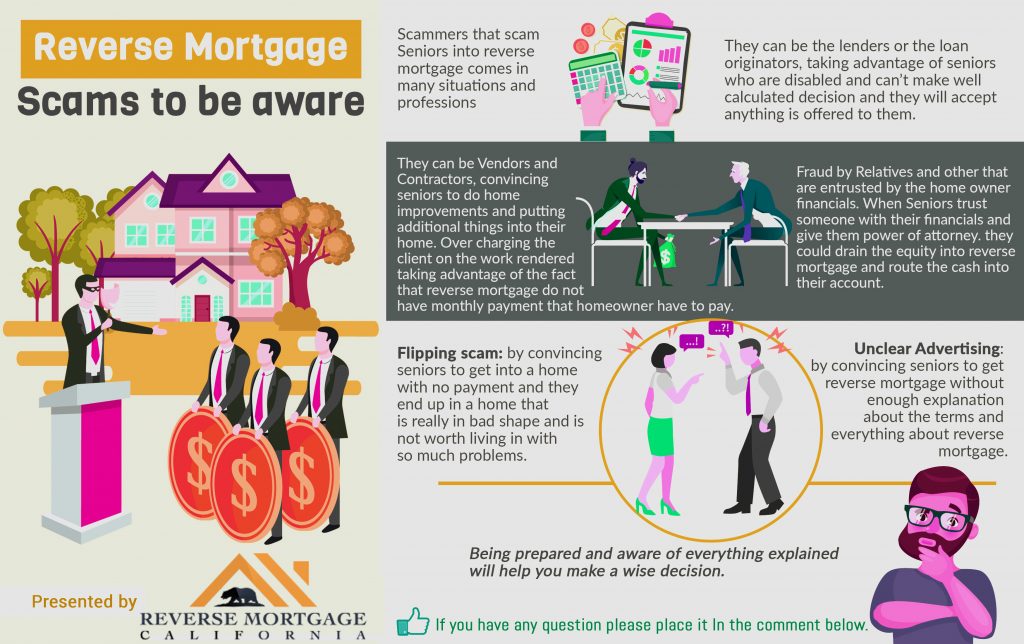

Reverse mortgage is potentially lucrative and vulnerable borrowers who might be desperate for finances or have cognitive impairments are prone to scam. Unscrupulous vendors target seniors offering help in securing reverse mortgage for pay. The vendor runs off with the money without delivering the promise.

Financial advisors, caregivers, and relatives in some cases take advantage of seniors using an attorney to steal proceeds or convincing them to purchase financial products including whole life insurance or an annuity that they can just afford through a reverse mortgage.

How to Avoid Foreclosure

A foreclosure is another danger of a reverse mortgage. The owner must meet various conditions, and failing to meet them gives the lender the right to foreclosure.

The borrower has to reside and maintain the home. If a homeowner gives up on good repair of the house, its value will be lower when reselling making it hard for the lender to recover the full amount extended to the homeowner. The borrower is required to be current on homeowners insurance and property taxes. The requirement protects the lender in case the collateral is damaged. Research shows that every one out of five reverse mortgages is caused by the homeowner’s failure to stay current on insurance and property taxes.

Loan Limit

Your payment plan and the lender determine the proceeds you receive. For the HECM, the borrowing limit is based on the youngest borrower’s age, the appraised value of your home, and the interest rate of the loan.

However, you can’t get 100% of the value of your home or anything close to it. Here are things you should know about the amount you can borrow:

• Loan proceeds are determined by the youngest borrower’s age or the younger spouse if married. The older the borrower, the higher the proceeds.

• A lower mortgage rate allows you to borrow more.

• The higher the appraise property value, the bigger the loan

• The stronger the reverse mortgage financial assessment, the more the proceeds

Your Heirs and Spouse

Both spouses must consent to the reverse mortgage even if both are not borrowers. This arrangement may create problems. If only one partner is listed as the borrower and they live together, the other spouse could lose the home if the listed partner dies first. When the borrower dies, the reverse mortgage needs to be repaid by selling the home. If the spouse chooses to keep the house, they must repay the loan.

Conclusion

For the senior homeowners who fully understand loans and trade-offs involved, getting a reverse mortgage could be a financial savior. Be sure to learn about how a reverse mortgage works if you are interested in taking on one. This way, you will make a sound decision and also avoid scam and poor- quality services.