Reverse mortgage net principal limit is the term used to denote the amount of money a reverse mortgage borrower can obtain after closing costs have been factored in and the loan has closed.

How much this is depending on several factors, particularly:

- The amount the borrower must pay for upfront fees

- The equity value of the home

What is a Reverse Mortgage?

Reverse mortgages use a borrower(s) property as secured collateral and are an alternative form of second mortgages. Although interest accrues over the life of the loan, no monthly payments are required. Instead, borrower(s) must repay the loan in its entirety if they sale the property or their estate must do so after their death.

Reverse mortgages can be customized to the borrower(s)’ specific needs. This includes deciding on a single payout with a fixed interest rate or monthly cash disbursements and lines of credit with variable interest rates.

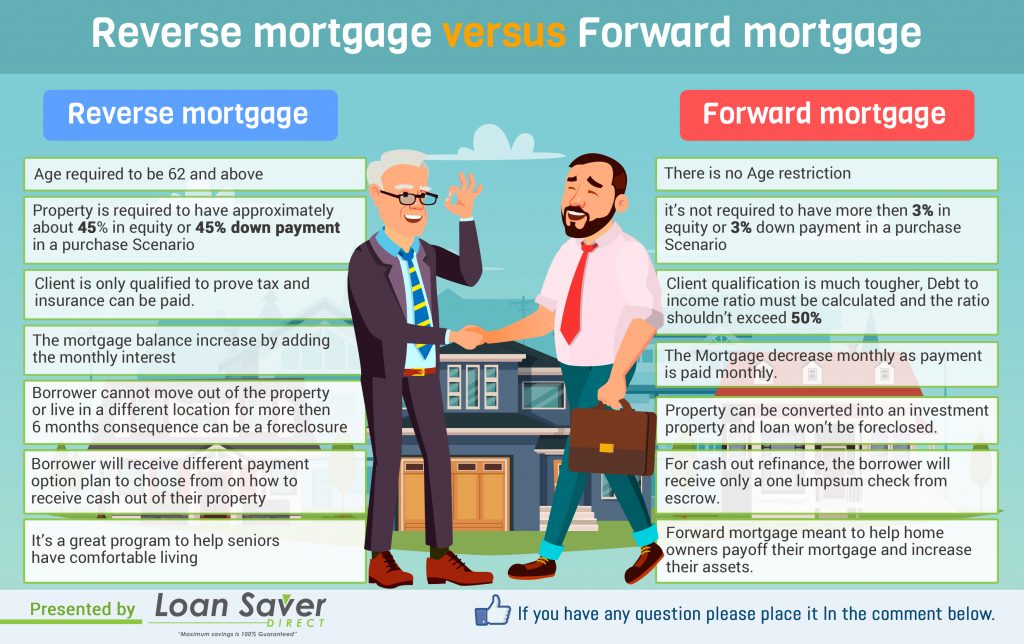

Who is Eligible for Reverse Mortgages?

Reverse mortgages, which may also be referred to as home equity conversion mortgages, are intended for homeowners who are 62 years old and older. Although the borrower(s) receive cash for their home’s equity, they are not required to make monthly payments on the loan. The borrower(s) can choose to have the equity amount given to them in a single lump sum or in installment amounts. This will be set while deciding on the terms of the loan.

The Federal Housing Administration, or FHA, sponsors reverse mortgages. Reverse mortgages are supported by the U.S. Department of Housing and Urban Development (HUD). Anyone considering a reverse mortgage can find FHA-approved lenders

Considerations for Net Principal Limit

Any borrower(s) interested in a reverse loan should apply with a FHA-sponsored lender. The lender will offer principal loan balances based on:

- The age of the borrower(s)

- The equity value in the home

- The appraised value of the home

Only borrowers age 62 and over should apply for a reverse mortgage. The principal balance cannot be more than FHA-sponsored limits. The FHA has set specific instructions for calculating principal offers. Borrower(s) are restricted to a certain amount during the course of their life.

The net principal limit may also be measured against the current net principal limit. The current net principal limit refers to the revolving balance available on the borrower’s account. At the beginning of the loan, the net principal limit and the current net principal limit will be the same amount.

Typically, borrows opt to pay the closing costs associated with a reverse mortgage using their principal balance. The amount remaining after closing costs have been paid is referred to as their net principal balance.

When taking out a reverse mortgage, borrowers can anticipate a variety of additional costs. They include the loan origination fee, home appraisal fees, the up-front mortgage insurance premium, and the cost of a home inspection.