You may or may not be familiar with the terms that the mortgage industry is using today. The two of the most recent involves the use of a forward mortgage and reverse mortgage. Determining which mortgage type is best for you will depend on the home loan that will suit your needs best. This is especially the case for those of you who are in a certain point in life, particularly when it is pertaining to your present personal and your financial position. Having said this, here is what you need to know about each.

Reverse Mortgage

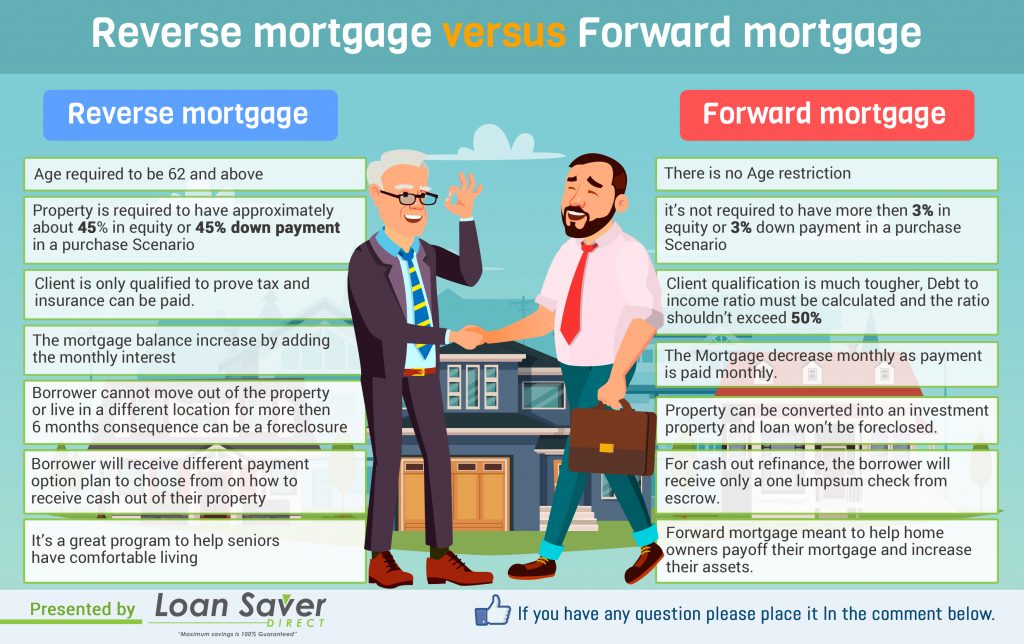

Before you can understand the information that you need to know on reverse mortgages, it is essential that you have a good basic idea of what this mortgage actually entails. First off, the person that applies for this type of loan must be at least 62 years of age or older. In fact, the older the age of the person, the more likely that the bank will approve the loan.

Similar to the home equity line of credit, the reverse mortgage is nearly the same in terms. For instance, if you apply for this type of mortgage, you will have a set amount that you can use for anything that you desire. This mortgage type is also available for you at any time. While the reverse mortgage may be very attractive for this reason alone, there are some drawbacks that you need to consider. One of the most and highest risks of obtaining this kind of mortgage is not having the capability to pay it back by a set amount of time. When this is the case, you may be in jeopardy of losing your home due to the principal amount borrowed and the added interest.

Embedded Risks in the Reverse Mortgage Option

While the reverse mortgage has some significant drawbacks for senior citizens, these loans are considered to be highly regulated by the Federal Government. However, if senior citizens do not want to be taken by the pitfalls in this loan, it is very important that everyone gets a detailed overview of what types of limitations that are inherently involved. Here are just a few.

Temptations for this loan is considered to be obvious for those who want to borrow the loan at a fixed rate to pay off any of their outstanding expenses.

A flexible rate mortgage is also a temptation that many homeowners may not be able to resist, unless they will listen to other borrows who are saying that this line of credit option in the loan can be difficult to pay back when it comes due.

If you decide to apply for the reverse mortgage, you may leave your family in a situation that is difficult to get out of. For instance, if you sign up for this loan, your family may be forced to pay a lump sum back before they can sell the family members home.

Forward Mortgage

Unlike the requirements of the reverse mortgage, the applicants that can apply and obtain an approval for this type of loan is not confined to the age requirements of 62 years of age and older but is available to homeowners of any age. For instance, the basic guidelines for the forward mortgage, however, is geared toward those who have already paid off their 30 year mortgage and would like to take advantage of a huge amount of their equity. In some cases, the individual or couple will be looking for a loan amount that may take them 10 or 15 years to repay this amount back. The amount of the mortgage and the interest rate is usually significantly lower so the owner may be looking at an attractive deal for getting the amount upfront that they owe.

Embedded Risks in the Forward Mortgage Option

The Forward Mortgage option has a certain amount of embedded risks too. Even though the homeowner may have a chance to whittle away at these new debt amounts, the financial capability to continue to pay these amounts back can be inherently risky as well. Here are a few scenarios that you need to consider prior to grabbing this opportunity.

- Forward mortgages loan amounts are based on the fact that property values will increase. Hence, when you are paying the loan back, the principal and interest are based on the newer value of the property as they increase over time. In short, you will be paying back an amount to your bank that is based on an inflated mortgage that can range as high as 25% more of the traditional home loan.

- Similar to the housing boom, these rates can be adversely adjusted any time. Thereby, leaving the forward mortgage loan borrower at risks of suffering the same fate of others that lost their homes. In short, if the homeowner is stuck in this situation, they may be left with an amount that exceeds the actual value of their property.

Takeaway

You need to make sure that you are armed with the facts for both the reverse mortgage and the forward mortgage so that you know the inherent risks of borrowing such a huge loan amount. By using your home as collateral, it may be financially advantageous now based on the stage in life that you are presently in. However, as the years go by and the money needs to be paid back, anything can happen that will place you and your family at a huge financial disadvantage in your latter years.