There are lots of financial con artists, but reverse mortgage scammers are considered among the worst if not the worst. That’s because they take advantage of their position as trusted lenders, advisors, or even professional contractors, to exploit seniors who need funds.

They trick the elderly into signing up for financial products, so much complicated that they won’t be understood even by well-educated, brilliant individuals, let alone those whose mental capability has been diminishing with age. After doing so, they get away with the proceeds and leave the homeowner with some debt or even at risk of losing their home.

Reverse mortgages can be good in some situations, but not others. There are times when this kind of financing can be the worst choice you ever made. That’s why we have crafted this article to let you know more about the most common reverse mortgage scams. This way, you can easily avoid them and warn others too, who may be potential victims.

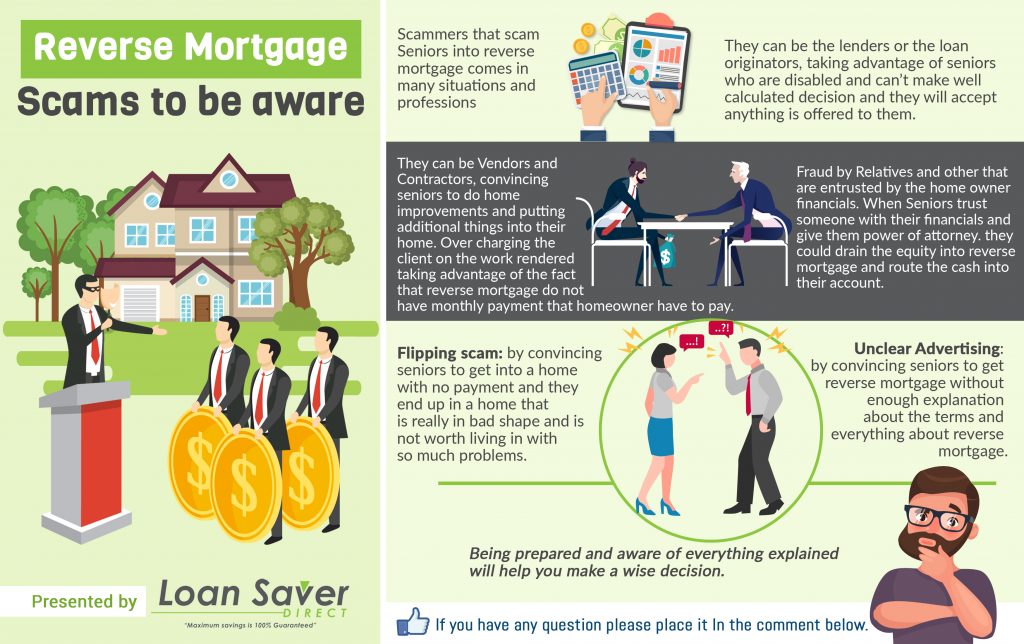

Vendor and contractor fraud

This scam involves targeting the elderly and interesting them in a home-improvement service such as a remodeling project, repair, or something else. If the elder shows interest in paying for such a service, the con suggests the ‘best’ solution – a reverse mortgage. As much as a reverse mortgage is an excellent way to pay a contractor or vendor, it might not be advantageous to the homeowner, and they may end up making a loss.

If you feel like your home needs some repair, but you are out of options when it comes to paying, getting a home equity loan or even opting for a home equity line of credit could be a better option. This is in consideration that it’s less expensive and has fewer consequences compared to a reverse mortgage. You should avoid listening and perhaps even working with a contractor who advices you to pay for the service provided using a reverse mortgage.

Fraud by relatives, others

This is somehow similar to the vendor and contractor fraud, in that someone tries to get you to purchase a financial product that you do not need. They try to convince you that what you need is a reverse mortgage to pay for the product with ease. Such people normally don’t have your best interests at heart, and will do anything to exploit you if you give them a chance.

You also have to be careful with Power of Attorney (POA) documents, as they give the holder power to complete financial activities on the owner’s behalf, taking out a reverse mortgage on their/your house included. This is quite common as seniors often want to entrust someone to manage financial affairs on their behalf. If the entrusted individual does not have good intentions, they may decide to secure reverse mortgages, and then divert proceeds to their accounts. In some cases, fraudsters have gone as far as successfully securing reverse mortgages for deceased relatives.

Flipping fraud

This reverse mortgage scam is all about seniors being tricked into buying a lower-cost home, which initially seems to be an impressive deal. The houses are, however, usually in poor condition, only that they have been given a facelift. The realtors who tricked a senior into purchasing the lower-cost home can then secure a “Home Equity Conversion Mortgage for purchase”, which is a special reverse mortgage. They then use the HECM to pay for the home and find a way to benefit fully from the proceedings by diverting the proceedings to their accounts. The seniors feel convinced that they are benefiting from a Housing and Urban Development program, which is usually not the case.

Robbing Peter to “pay” Paul

For such a scam, trusted entities such as an insurance company fail to transmit money meant to pay lenders from part of the homeowner’s mortgage proceeds. In 2009, an insurance company in Orlando confessed to stealing mortgage proceeds which amounted to $1 million in such a type of scam. The mortgage holders thought that part of their proceeds were being used to reduce their debt as well as increase their home equity. Things turned sour when they finally ended up in foreclosure after “defaulting” on their mortgage payments.

Additional misleading tricks

There are other misleading tricks which even though are not aimed at stealing money from potential homeowners, do not benefit them in any way. Here are the main ones:

- High-pressure sales

These kinds of sales may not be frauds, but one thing you are sure of is that they are not in any way meant to make things easier for you. Taking out a reverse mortgage is a serious decision that needs a careful consideration and understanding of the terms involved. If you feel that a reverse mortgage lender is pushing you into making a quick decision, ignore them, and find another one. Besides, you can also cancel a reverse mortgage deal within three business days if you feel that it won’t work for you. To do so, you will have to notify your lender in writing before the three-day period comes to an end.

- Unclear advertising

There are lots of adverts that convince homeowners to take out a reverse mortgage without clearly stating the terms and consequences of not observing the terms that have been set. In some cases, a homeowner is also promised financial security and assured that their home is under no risk, while that is not the case.

The Consumer Financial Protection Bureau (CFPB) released a report stating that many of the mortgage adverts it analyzed have unclear information regarding requirements, insurance, and associated risks. The CFPB, after organizing a focus-group interview with homeowners who qualified for reverse mortgages found out that some lenders create a false sense of security about such mortgages. Some of them don’t even want to make it clear that reverse mortgages are loans. They also make it look like a homeowner can’t lose their home, which is far from the truth. In some cases, a lender may also make a homeowner believe that the government funds reverse mortgages, which is also misleading information. However, it should be clear that the Federal Housing Administration insures Home Equity Conversion Mortgages.

To sum it all,

Some reverse mortgage scammers are somehow lucky that the law has not caught up with them yet. That’s why you never want to be ignorant of the existent reverse mortgage scams, as the fraudsters are always targeting anyone who is not well informed on such issues. You should be so much cautious about anyone who tries to convince you to take out a reverse mortgage loan, even if the deal seems to be the best. Consider conducting deep research and getting financial advice first before making a decision, as that can save you from getting scammed.