Reverse mortgages have been severally advertised as able to provide homeowners with a secure source of income for the rest of their lives. While the claim may be true depending on the conditions, there are some risks associated with such a kind of loan. One of the main risks is running out of proceeds earlier than expected. These loans – for those who may not be very familiar with them – allow homeowners with a certain home equity value to borrow against such a value.

You can choose from six different ways of receiving mortgage proceeds. You should, however, keep in mind that the method you choose can affect how quickly and easily you lose your ability to borrow against your home equity value. Here are the six most common ways to receive your mortgage:

- Term reverse mortgage

- Fixed-rate lump sum

- Tenure reverse mortgage

- Modified term reverse mortgage

- Line of credit

- Modified tenure reverse mortgage

All of the six options listed above have different risks associated with them, which is why borrowers need to be cautious. To help you make a better decision, we have discussed the different scenarios in which one can run out of their proceeds earlier than expected, and how to avoid such a situation:

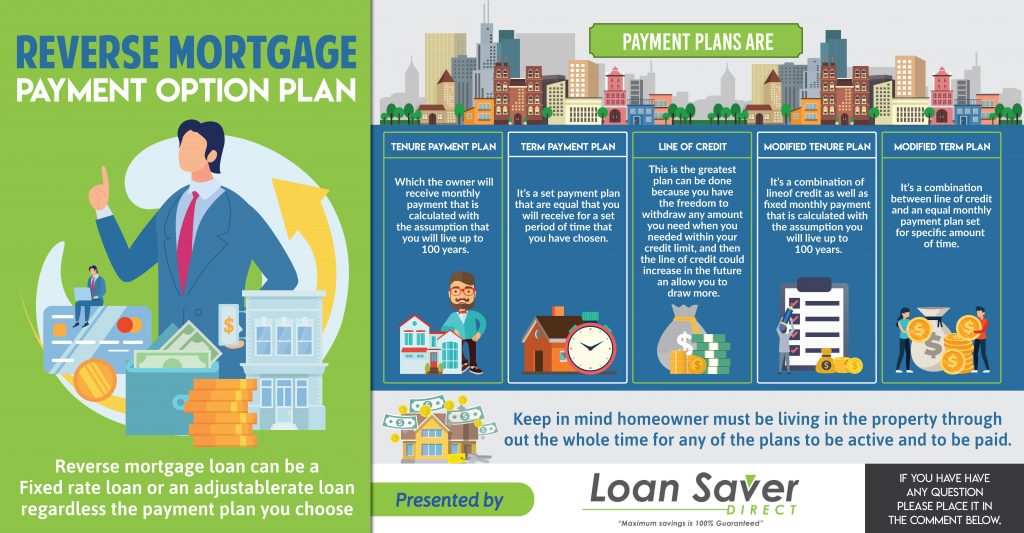

Term reverse mortgage

This payment plan allows homeowners to get equal monthly payments, which are then stopped at a pre-determined date. Once you have reached the principal limit of your loan, which is the maximum amount you can borrow, the proceeds from your reverse mortgage will be stopped. You can, however, continue living in the house, as long as you continue paying ongoing taxes and maintenance.

Fixed-rate lump sum

This payment plan for reverse mortgages comes with a fixed interest rate. Having a fixed interest rate for a fixed sum can be a low-risk way to borrow, but not with a reverse mortgage. This is in consideration that most homeowners opt for reverse mortgages when their home’s equity is the only option they have for acquiring the cash they need.

If, however, a homeowner takes out such a loan and fails to plan adequately for it, they can mismanage the cash and be left with no monetary sources to secure them financially. The Consumer Financial Protection Bureau (CFPB) has made it known that the lump sum option, which is becoming popular as time goes by, is a risky option. This is especially true for younger borrowers, considering that most have longer lifespans and may not have additional retirement resources. As such, most of these young borrowers end up using their equity in early retirement.

You, however, have the option to continue staying in your home even after having exhausted the proceeds. The only problem is that one may find it hard paying for their living expenses and can as well end up in foreclosure. This is in consideration that one has to continue paying their homeowner insurance and taxes, as well as paying for the maintenance of the house to continue having the reverse mortgage.

The CFPB noted that fixed rate borrowers have a higher risk of defaulting on their reverse mortgages due to the expenses involved compared to borrowers with an adjustable rate. Besides, the lump sum involved in such a payment plan can easily attract greedy relatives as well as scammers who may want to benefit from the same.

Tenure reverse mortgage

This plan does not have a considerably high risk of running out of cash. This is, however, requires the homeowner to continue settling their home repairs, insurance, and tax bills. Failure to do so can lead to the loan becoming due and payable.

The tenure payment plan allows for an adjustable interest rate and equal monthly payments during one’s entire life. This is, however, on condition that at least one of the borrower permanently resides in the home.

Modified term reverse mortgage

This plan offers a fixed monthly payment and access to a line of credit over a predetermined number of months. The monthly payment depends on the chosen term plan, while the line of credit depends on the line of credit plan that you have decided to go with.

With a modified term plan, your monthly payments should be available for a predetermined period even though the line of credit will still be available until you exhaust it. The best thing you can do to avoid running out of cash with this plan is using your line of credit with care. You should also do your best to avoid exhausting the line of credit early as that may also make you run out of money quickly.

The best choice you have is to use only the term payments until the term ends as you let the line of credit increase. Once the term comes to an end, you can then use the line of credit without much to worry about. You can also build up enough equity to get the flexibility to sell your property, clear the loan, and move as long as you haven’t used the line of credit.

Line of credit

How you use, this plan is what determines how quickly and easily you can run out of money. This plan, unlike a home-equity line of credit (HELOC), cannot be canceled or reduced even when there are changes in the home value or your finances. This irrevocable status lowers the risk of losing access to money.

Besides, the available line of credit will only lower as you draw upon it, and the interest and mortgage insurance premiums are only on the cash you borrow. You also get access to more funds with time, considering that the unused line of credit increases every year whether or not your home’s value is increasing. The unused part of your line of credit will grow at a rate similar to what you are paying on the cash you borrowed.

You are allowed to access a maximum of 60% of the principal limit during the first year. You can then draw on the other 40% for the second year going on, in addition to what you didn’t use during the first year. Using up the available line of credit early will leave you with almost nothing to use for years to come unless you decide to pay the entire amount of what you borrowed. This is in consideration that there is no prepayment penalty for paying to reduce your reverse mortgage balance.

Modified tenure reverse mortgage

This plan offers fixed monthly payments and a line of credits as well. The monthly payment amount depends on the tenure plan while the line of credit plan determines the line of credit amount. You can opt not to use the line of credit, as that will make you owe less. That should be a good choice for a homeowner who wishes to have assured income as long as they are alive without having to risk depleting their equity hence being unable to move.

How to avoid running out of proceeds

To avoid running out of proceeds so early, once should consider waiting as long as they can as that lowers the chances of outliving proceeds. The CFPB states that younger retirees may be at risk of using up their entire home’s equity if they chose a reverse mortgage. That may, however, not be a problem if they plan to stay in their current home for life.

Another thing you also need to consider is that an increase in interest rates can decrease the amount available for you to borrow even if you are older. This was verified after Jack M. Guttentag, a finance professor at Wharton School of the University of Pennsylvania researched the subject.

His findings were that a 62-year-old who chose to go with a line of credit plan could have their credit line go up by 17% if they waited for 10 years to get a reverse mortgage. That was, however, on the condition that interest rates do not change.

If the rates doubled, the same individual would only have access to a 69% smaller line. As such, it may be preferable that one takes out a reverse mortgage line of credit plan early and then avoid touching the line for as long as they can to maximize the growth potential.

Making changes to your current plan

If you have a reverse mortgage plan already and you like you are at risk of running out of proceeds earlier than desired, you may want to talk about it with your lender. It is possible to changes your payment plan, as long as you didn’t opt for the lump sum option for your reverse mortgage. You are also required to stay within the principal limit for this option to work. If, however, you qualify to change your payment plan, then you may want to consider doing so since it only requires that you pay a $20 administrative fee and is much simpler than refinancing.

Non-borrowing spouse dilemma

No matter what payment plan you opt for, having a younger non-borrowing spouse may mean that they are at a higher risk of outliving the proceeds if you die first. A law that came into effect in 2015 protects any qualified non-borrowing spouse from moving out should their fiancée predecease them. The non-borrowing spouse, however, will not receive additional payments once the borrower passes on.

Depending on the house’s worth and the loan balance, however, the non-borrowing spouse may be in a position to sell the property and clear the reverse mortgage. But that can leave them with

not enough cash to depend on. If, however, they have enough income to secure a regular forward mortgage, they may be able to refinance out of the reverse mortgage.

Keep in mind that if the reverse mortgage balance is more than the home’s value, it should be best for the non-borrowing spouse to continue living there. This is in consideration that selling it can live them with no cash and no place to call home.

Final Remarks

Most of the reverse mortgage adverts seem to lead seniors into believing that they won’t outlive their proceeds. That’s, however, not the case, which is why it’s important to understand all the conditions under which a reverse mortgage may not offer financial security in one’s lifetime before taking out such a loan. The information above should make it easier for you to determine whether such a type of loan can work well for you and if it does, which plan should be the best.